Does the Fed taper even matter anymore?

November or December, who cares?

Next week is Fed week and that means we’re going to be hearing plenty about tapering.

I tend to file it all under ‘noise’. At this point, the Fed debate revolves around announcing a taper in November or December. The difference is negligible.

The next argument is the size and pace of the taper. The parameters on that are settling around a six-month, eight-month or twelve-month timeline to halt purchases.

I’d also argue that this also doesn’t really matter, particularly since the Fed is now going to great lengths to disassociate tapering with liftoff. I think the market’s gotten that message.

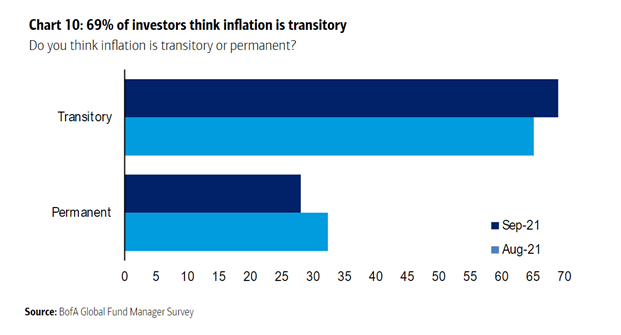

So if we zoom out, the only real thing that matters is the date of liftoff and that’s a circular argument back to inflation. Lately, team transitory is winning, as shown by the BofA hedge fund manager survey:

Will that continue? It depends on the data. This week CPI numbers were low and that will give the Fed a bit more confidence on staying patient. But what the future holds is highly uncertain and I think that’s why markets continue to bob around.

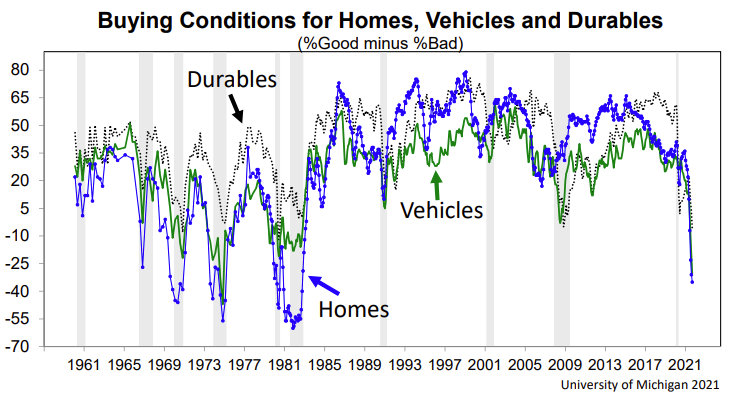

Will that continue? It depends on the data. This week CPI numbers were low and that will give the Fed a bit more confidence on staying patient. But what the future holds is highly uncertain and I think that’s why markets continue to bob around.More at the top of mind is how demand will develop as bottlenecks crimp supply and push up pricing. Today’s UMich sentiment survey showed terrible buying intentions for durable goods, cars and houses.

Globally is where the largest worries lie. The eyes of all veteran market participants gloss over at the idea of a China crisis or pronounced slowdown because we’ve been hearing it for 20 years but Evergrande and common prosperity is something new.

Globally is where the largest worries lie. The eyes of all veteran market participants gloss over at the idea of a China crisis or pronounced slowdown because we’ve been hearing it for 20 years but Evergrande and common prosperity is something new.So while we’re all focused on the FOMC next week, it may be the PBOC that steals the show.