Payment stock ‘winners’ come down to earth and other 2022 insights: Bernstein (NYSE:MA)

Nattakorn Maneerat/iStock via Getty Images

Bernstein analyst Harshita Rawat distills Q4 2021 and the beginning of 2022 down to 10 key insights in assessing U.S. payments stocks. The top one: “‘pandemic & stimulus’ tinted glasses are coming off, bringing some ‘winners’ down to earth.”

Overall, Visa (NYSE:V) and Mastercard (NYSE:MA) are the most likely within Rawat’s coverage to see positive revisions and “improvement in narrative”. And while Russia domestic exposure is manageable for both companies, “we are closely watching domino effects in cross-border travel.”

The nine other key insights are:

- “Not all customers are created equal, we are closely watching customer acquisition costs (and potentially deteriorating unit economics) in a post-pandemic world.”

- “Networks are here to stay. Revenue through scaled partnership & customer engagement beat modest savings on card expenses.”

- Expect another round of deal-making/M&A — “Likely buyers: merchant acquirers (both legacy & new age).” Focus areas are Buy Now, Pay Later consolidation, business-to-business expansion, bill pay, ecommerce “power grab, geo expansion, software, crypto.”

- Inflation will help revenue of most payment stocks. For example, Visa (V), Mastercard (MA) and acquirers’ revenue are linked to transaction values. But it’s a negative for companies relying on consumers’ discretionary spending, like PayPal (NASDAQ:PYPL).

- “Ecommerce wars are beginning amid deceleration, shrinking low-hanging fruit opportunities and changing market landscape.”

- Crypto is a friend (even if complicated) but not a foe.” Rawat points out that cryptocurrency is a feature, not a bug, in that it drives user engagement and monetization.

- Rawat gives big tech credit for persistence in payments, but sees their threat as likely overblown.

- Account-to-account is “still the biggest threat we are watching but we are sleeping a tiny bit better at night.” A2A critical features such as request-to-pay, variable recurring payments, and chargebacks are lacking, Rawat said.

- Lastly, she asks whether tech and fins are starting a “great convergence.” Rawat is closely watching the start of rewards on such channels as PayPal (PYPL) and BNPL and “some leveling of the playing field as in the BNPL space.

Rawat also likes Block (NYSE:SQ) for its Cash App clearing event, efficient customer acquisition model vs. its peers, and Afterpay deal integration.

Meanwhile, PayPal’s (PYPL) risk reward is likely to improve a ecommerce deceleration is now well-understood and expectations have been reset lower. Execution and competition will be key.

Acquirers Fiserv (NASDAQ:FISV) and Global Payment (NYSE:GPN) are seen as tactical recovery and valuation trades.

Looking at a group of payment stocks, Visa (V) and Mastercard (MA) also rate the highest by SA Quant rating. Affirm Holdings (NASDAQ:AFRM) and Lightspeed Commerce (NYSE:LSPD) screen poorly.

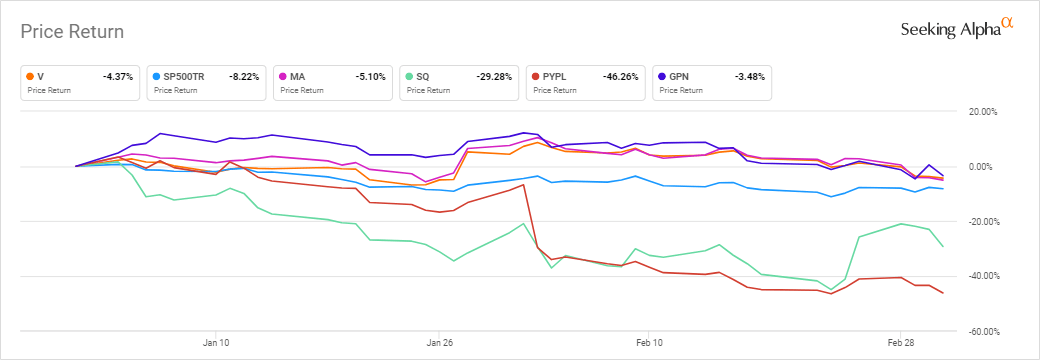

YTD, Visa (V), Mastercard (MA) and Global Payments (GPN) stocks fall less than the S&P 500, while Block (SQ) and PayPal (PYPL) both dropped more than the broader index as seen in the graph below.

Previously (Feb. 2), PayPal, Block, other fintech stocks returned to earth after PYPL pivoted on its customer acquisition strategy